- Published on

The Great Divergence: Why SaaS Costs Are Outpacing Wages — And What It Means for Your Business

- Authors

- Name

- Anablock

AI Insights & Innovations

The Great Divergence: Why SaaS Costs Are Outpacing Wages — And What It Means for Your Business

March 2026 | Economic Intelligence Report

Executive Summary

A quiet financial crisis is unfolding inside corporate budgets. While wages have moderated to their most stable levels since the pre-pandemic era, SaaS vendors are raising prices at 3 to 5 times the rate of general inflation. The result: a widening gap that is squeezing IT budgets, frustrating procurement teams, and creating a once-in-a-decade opportunity for cost-efficient software alternatives.

This report draws on live Federal Reserve FRED data, BLS Employment Cost Index figures, and current SaaS pricing intelligence to give you a complete picture — and a strategic playbook.

Part 1: The Wage Inflation Story — Moderation Has Arrived

Average Hourly Earnings (FRED Series: AHETPI)

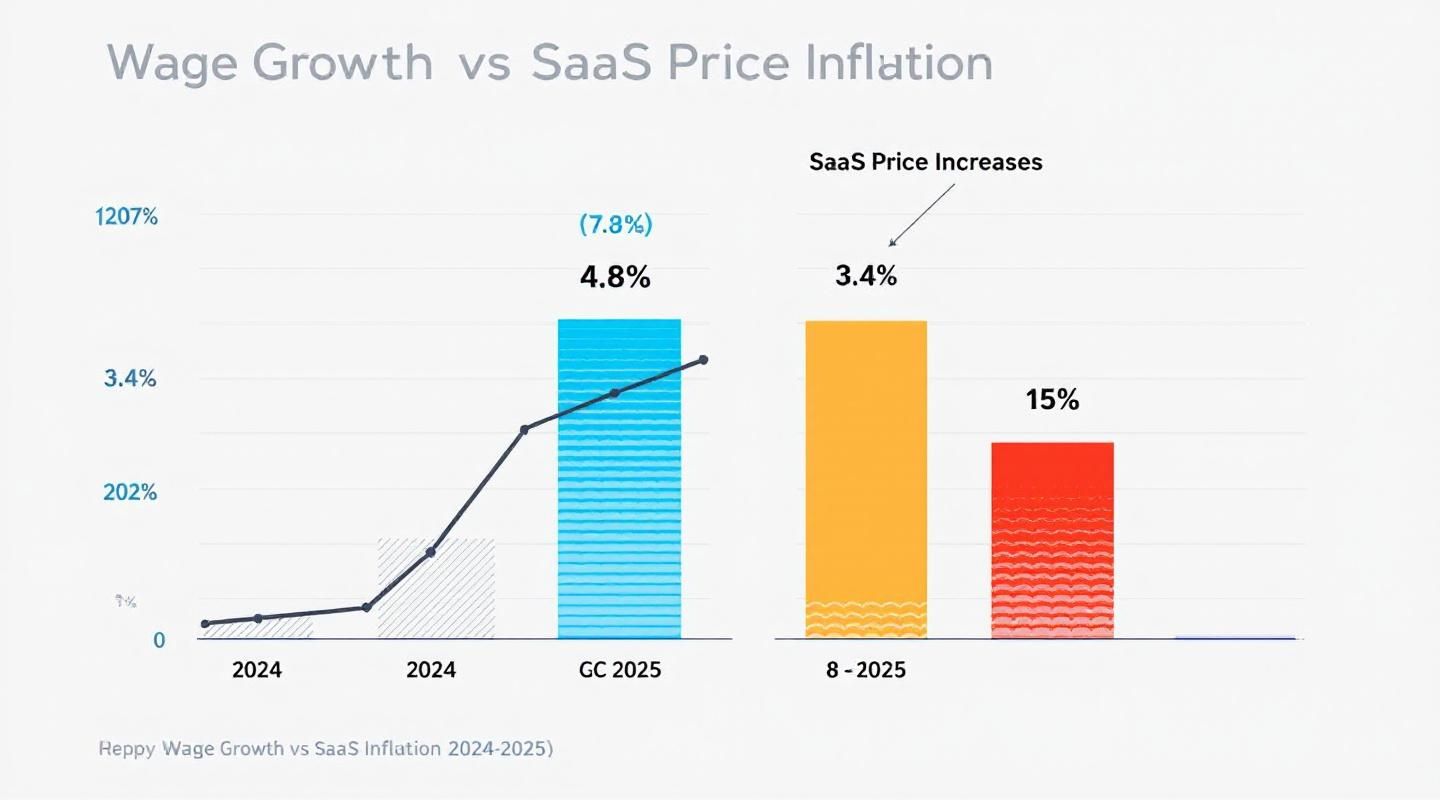

The post-COVID wage surge is definitively over. After peaking at +6.9% year-over-year in early 2022, average hourly earnings growth has decelerated steadily and now sits at +3.8% as of February 2026.

| Period | Avg. Hourly Earnings | YoY Growth | |---|---|---| | Jan 2021 | $25.16 | — | | Jan 2022 | $26.91 | +6.9% | | Jan 2023 | $28.31 | +5.2% | | Jan 2024 | $29.61 | +4.6% | | Jan 2025 | $30.79 | +4.0% | | Feb 2026 | $32.03 | +3.8% |

Source: Federal Reserve Bank of St. Louis, FRED Series AHETPI

Employment Cost Index (ECI) — The Deeper Picture

The BLS Employment Cost Index, which captures total compensation including benefits, tells an even more striking story of deceleration:

| Quarter Ending | Wages & Salaries (YoY) | Total Compensation (YoY) | |---|---|---| | Mar 2024 | 4.1% | 4.8% | | Sep 2024 | 3.6% | 4.7% | | Dec 2024 | 3.6% | 4.7% | | Jun 2025 | 3.5% | 4.0% | | Dec 2025 | 3.3% | 3.4% |

Source: U.S. Bureau of Labor Statistics, Employment Cost Index Q4 2025

Key insight: Real (inflation-adjusted) wage growth is now only +0.7% — workers are barely keeping pace with CPI at 2.4%. The labor market has normalized.

Part 2: The SaaS Pricing Story — Acceleration Continues

While wages have cooled, SaaS vendors have done the opposite. The data is stark:

The Numbers at a Glance

| Metric | Rate | |---|---| | Wage inflation (ECI, Dec 2025) | 3.3% | | CPI / General inflation | 2.4% | | Average SaaS price increases | 8–12% annually | | Aggressive SaaS vendors | 15–25% | | SaaS cost per employee (2025) | ~$9,100 (up from $7,900 in 2023) |

SaaS inflation is running 3–5× faster than wages. Over just two years, the average organization's per-employee SaaS spend has grown nearly 15% — while the workforce's purchasing power has barely moved.

Major Vendor Price Increases (2025–2026)

The increases aren't theoretical. Here's what's actually happening in the market:

| Vendor | Increase | Effective Date | |---|---|---| | Salesforce | +6% on Enterprise & Unlimited editions | August 2025 | | Adobe Creative Cloud | ~27% effective increase via restructuring | June 2025 | | ServiceNow | 5–10% base + 30–45% premium for AI add-ons | 2025 | | Microsoft 365 Business Standard | $12.50 → $14.50/user/month | July 2026 | | Slack Business+ | Now $18/user/month | June 2025 |

Hidden inflation alert: 60% of vendors are masking price increases through credit systems, bundled features, and AI add-on premiums — making true cost visibility increasingly difficult.

Part 3: The Strategic Implications

🔴 For SaaS Buyers

The math is unambiguous: your SaaS stack is growing more expensive at a rate your payroll budget cannot match. This creates three urgent priorities:

1. Audit for SaaS sprawl. With the average employee costing $9,100/year in software alone, unused licenses are pure waste. A 10% reduction in unused seats across a 500-person company saves ~$455,000 annually.

2. Renegotiate before renewals. Vendors are raising prices on renewal — but they're also offering discounts to retain customers who push back. The window to negotiate is before the renewal notice arrives.

3. Evaluate alternatives. Buyer frustration is at a peak. 50% of software companies are preparing further price increases, and 60% are masking them. This is the ideal environment to evaluate competitive alternatives.

🟢 For SaaS Sellers

The wage moderation story is actually a selling opportunity — if you frame it correctly:

The ROI argument still works. At $32/hour average wages, software that saves even 2 hours per employee per week delivers $3,328/year in labor value per seat. That easily justifies most SaaS price points.

AI monetization is the growth lever. ServiceNow, GitHub Copilot, and Microsoft Copilot are all demonstrating that buyers will pay 30–45% premiums for AI features that demonstrably reduce headcount or accelerate output.

Target budget-fatigued buyers. Organizations that went CLOSED_LOST 12–18 months ago due to pricing may now be more receptive — their incumbent vendors have since raised prices, eroding the cost advantage that kept them away.

Part 4: The Macro Context — Why This Divergence Persists

The wage-SaaS gap isn't accidental. Three structural forces are driving it:

1. AI Investment Costs Are Being Passed to Customers

Every major SaaS vendor is investing billions in AI infrastructure. Those costs are being monetized through price increases and premium add-ons. Unlike traditional software features, AI capabilities are being priced as separate line items — creating effective price increases of 20–30% for customers who adopt them.

2. Vendor Consolidation Reduces Competition

The SaaS market has consolidated significantly. Fewer competitive alternatives mean less pricing pressure. When Salesforce raises prices 6%, most enterprise customers don't have a credible migration path — and vendors know it.

3. Switching Costs Are High and Rising

Data lock-in, integration complexity, and workflow dependencies make switching painful. Vendors are exploiting this by raising prices incrementally — small enough to avoid triggering a migration decision, large enough to compound significantly over time.

Part 5: What to Watch in 2026

Wage growth outlook: Analysts expect ECI to ease toward 3.5% in H2 2026 amid subdued labor demand. The next BLS ECI release (Q1 2026 data) is scheduled for April 30, 2026.

SaaS pricing outlook: With 50% of vendors preparing further increases and AI monetization still in early innings, expect average SaaS inflation to remain in the 8–12% range through 2026.

The opportunity window: The gap between wage growth and SaaS inflation is at its widest point in a decade. Organizations that act now — auditing, renegotiating, and consolidating — will build a structural cost advantage over competitors who don't.

Conclusion: The Divergence Is Your Competitive Edge

The data tells a clear story. Wages have normalized. SaaS costs have not. The organizations that recognize this divergence and act strategically — whether as buyers renegotiating contracts or sellers repositioning their ROI narrative — will emerge with a meaningful advantage.

The question isn't whether SaaS costs are rising faster than wages. They are. The question is: what are you doing about it?

Data sources: Federal Reserve FRED (AHETPI series), BLS Employment Cost Index Q4 2025, SaaS pricing intelligence (March 2026). All figures current as of March 15, 2026.